Efficient Markets Hypothesis

“A market where there are large number of rational, profit maximizers actively competing, with each other trying to predict future market values of individuals securities and where important current information is almost available to all participants” Eugene Fama on Efficient Markets

The theory of random walk led to the efficient market hypothesis. Eugene Fama, the father of modern mathematical finance, is one of the most brilliant economists of the modern era. A Nobel Laureate, Eugene’s work on efficient market hypothesis and asset pricing are crucial in determining modern portfolio theory. The Efficient Market Hypothesis presumes markets are informationally efficient. The theory proposes that current security prices reflect all the available information. The Theory of Random Walk is the underlying concept defining the Efficient Market Hypothesis. To understand the concept of efficient markets, lets look at the beginnings’ of Wall Street. Efficient Markets Hypothesis is key to understand Capital Asset Pricing Model.

Image: The middle Road

Capital Ideas, The Improbable Origins of Modern Wall Street

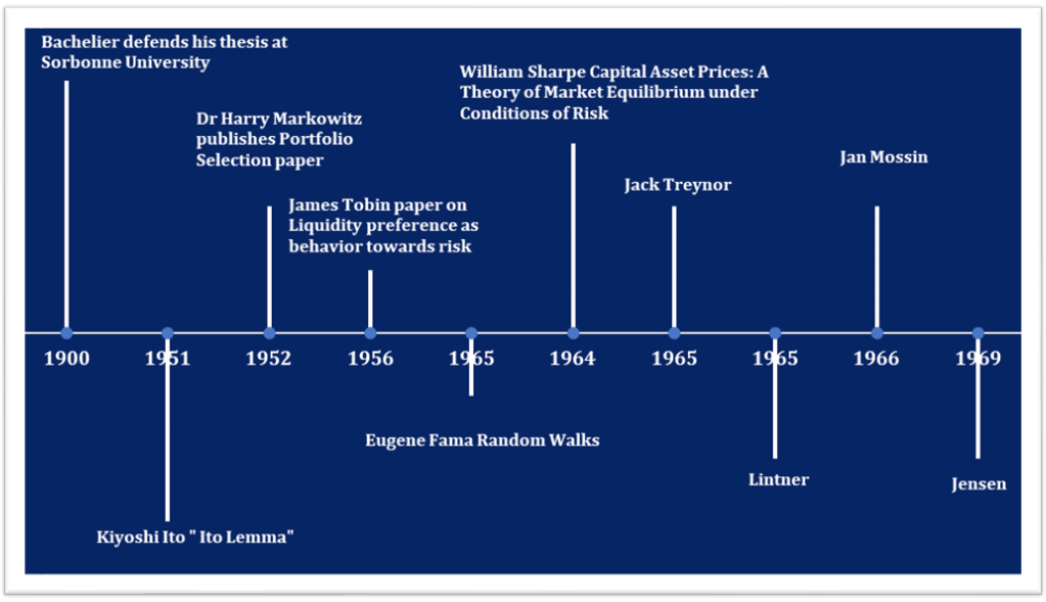

The book is a highly recommended read on the origins of finance on Wall Street. Written by the Wall Street Guru Peter Bernstein, the book traces the advent of mathematical finance leading to the evolution of the models in risk, valuation, portfolio management, and capital market pricing that define investment management today. The book captures the role of various actors within the business ecosystem — economists, mathematicians, statisticians, professionals and technicians in understanding and quantifying capital pricing models, among others, within the terminology of investment valuation. The book covers financial innovation from 1900 until the modern era of finance. The beginning of the mathematical foundation is credited to the Frenchman Bachelier, whose work defined the first known underpinnings of the Brownian movement within the financial jargon. Also known as a random walk, the Theory of Random Walk was made famous by the brilliant Nobel Laureate Eugene Fama; it is Bachelier who is credited to be the first to develop the stochastic process to analyze the random movement of stock prices. Any variable whose price uncertainly changes over time follows Stochastic Process. Variables are either continuous in time or discreet. Stock market prices are continuous in time.

Markov process is a type of stochastic process where only the current value of a variable is important for predicting the future-follows the weak form of efficient markets.

Bachelier was also the first to use a theoretical model to price options and futures in 1900. Through his research, he discovered that every time the price of an asset moves, the speculator has an equal opportunity to either win or lose, which led to the understanding that the mathematical expectation of the speculator is zero. He further quantified his findings that the price fluctuation of the market increase with time – the range within which the stock prices tend to fluctuate will increase as the square root of the time interval. This led to a better understanding of how security prices move, leading to the Efficient Market Hypothesis. Dr. Harry Markowitz, Father of Modern Portfolio Theory, seminal paper Portfolio Section set the ball rolling for quantifying risk and expected return. His key tenet that risk plays a fundamental role in investing led to the mean-variance portfolio. Variance is the measure of risk for a portfolio, square of the standard deviation of the portfolio. Investors decide on investments based on expected return and risk, which means the unit measure of risk in an asset defines the expected return. His work that any asset or portfolio is efficient if it offers higher or expected returns for the same or lower risk or the same or higher expected return for lower risk was intuitive in defining how investors perceive risk and expected return. Sharpe’s work quantifies risk-adjusted return, and Treynor is exemplary in quantifying the unit of risk to the expected return. Treynor’s ratio measures the excess of expected return over risk-free rate divided by beta to understand a portfolio’s systemic risk-adjusted return.

Dr. Harry Markowitz and Sharpe won the Nobel prize for their work in capital market theory and portfolio theory.

Efficient Markets Assumptions

- Investors want to maximize profits; are large and independent of each other

- Information comes out in a random, independent and unpredictable fashion

- Markets adjust rapidly to the information available under or over adjust over the short time

Types of Efficient Markets

There are Three Types of Efficient Markets

The weak form implies that the past rate has no bearing on future returns. Current stock prices fully reflect all security market information. Technical analysis has no relevance for predicting stock prices. In the semi-strong form of the efficient market hypothesis, current stock prices reflect past and public prices. This type of market fundamental market analysis will not give a decisive edge to predict stock winners. Public and private information is priced for valuing stock prices in a solid, efficient market. According to the Efficient Markets Hypothesis, an active investing style might generate higher returns due to anomalies in the market. Still, it is impossible to generate higher returns over the long term through an active investment management style. Passive funds will outperform active funds over the long term. Between 2009 to 2018, passive funds outperformed active funds on average, except PE, based on research by Deloitte. In recent years, the surge in passive investment suggests growing evidence within the investment management of a tilt toward a preference for a passive investment style. Yet there are instances of star investment managers example Peter Lynch, who have consistently outperformed the equity market.

Are we fooled by randomness?

References

- Capital Ideas, The Improbable Origins of Modern Wall Street Peter Bernstein